SBA 504

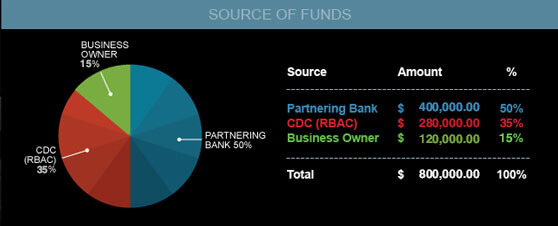

The US Small Business Administration 504 Loan or Certified Development Company ( CDC) program is designed to provide financing for the purchase of fixed assets, which usually means real estate, buildings and machinery, at below market rates. As part of RBAC’s mission to promote the economic development and the growth of businesses. The 504 program is a participation program that allows RBAC to partner with other financial institutions to allow the business owner to purchase the fixed assets that will help their business with little money down. The business owner puts a minimum of 10%, a conventional lender (typically a bank) puts up 50%, and RBAC puts up the remaining 40%. The maximum RBAC loan portion amount is $5.5 million ($5 million for meeting SBA-defined policy goals, and $5.5 million for manufacturers and some energy-related policy goals).